Bearer bonds flew across borders in one handshake but hid every owner. Traveler’s checks revealed identity and slowed to branch hours. Debit cards pushed checks onto networks, yet funds still crawled through fee-laden batch files.

Stablecoins close the loop; instant, programmable dollars whose public trail proves integrity without exposing personal details at every hop. They’re not new money, just the speed-plus-privacy ideal finally executed in code.

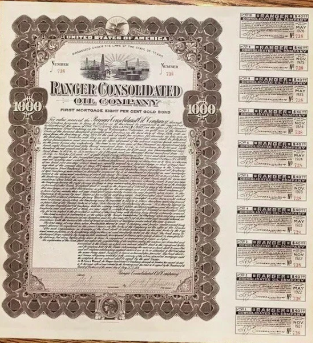

Bearer Bonds, Speed Without Identity

Bearer bonds offered 24/7, instant settlement and total anonymity. The moment the paper changed hands, ownership cleared with no registrar in sight. That round-the-clock speed thrilled investors while shoving compliance entirely off the playing field.

Each bond carried an engraved certificate number and detachable interest coupons that you clipped with scissors. Clearing houses tracked numbers in leather-bound ledgers, but ownership changed the instant the certificate crossed a desk, no telegraph or stamp required.

“Bearer bonds were the 19th-century USB stick. Plug-and-play liquidity you could slip across any border, no password required.”

What They Solved: Liquidity in a Handshake World

Capital markets of the late-19th century wanted value to move faster than ledgers or telegraphs allowed. The bearer bond emerged to fill that gap: a paper certificate whose possessor, not a name in a registry, held legal ownership. Hand the bond to another party and the deal was done; no bank clerk, no transfer agent, no waiting.

Speed didn’t stop at the principal. Interest payments were just as frictionless: holders clipped a physical coupon, presented it, and walked away with cash. The process removed custodial risk and intermediary fees, delivering predictable yield with minimal friction.

Because ownership rode on possession alone, bearer bonds provided rare cross-border neutrality. Bearer bonds were denominated primarily in currency, some with gold clauses, they could circulate across empires and through wars without needing conversion or local banking access.

The anonymity that made them so valuable proved to be their greatest weakness. Bearer bonds were welcomed by legitimate investors seeking privacy, but coveted by those eager to hide assets. For a world chasing instantaneous liquidity, they proved that money could, at least briefly, sprint ahead of the infrastructure built to track it.

What Still Broke: The Anonymity Tax

Bearer bonds’ blank-slate ownership quickly became catnip for tax evaders and money-launderers. With no registry and cash coupons paid to whoever clipped them, the certificates offered a ready‐made tunnel for unreported income and cross-border capital flight.

That same invisibility created “pocket risk.” Lose the certificate, or if it is stolen, the wealth was gone forever. Insurers priced the peril accordingly.

Regulators finally shut the door: the United States stopped new issuance in the 1982 Tax Equity and Fiscal Responsibility Act, and Europe adopted similar bans, drying up fresh supply and pushing most bearer paper into collectors’ drawers.

The reputation crystallized in pop culture. Hans Gruber’s $640 million score in Die Hard and Netflix’s $7 billion vault job in Kaleidoscope both hinge on bearer bonds precisely because they are untraceable and instantly negotiable.

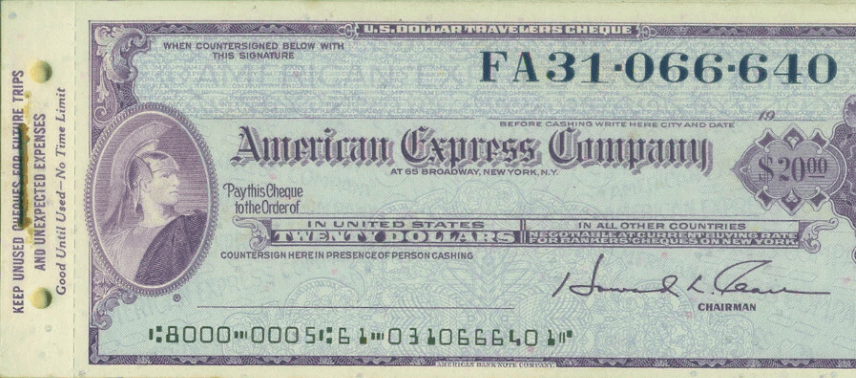

Travelers' Checks; Trust Without Velocity

American Express supplied the credibility; the branch clock dictated the pace. Each check cleared only when a clerk verified the countersignature, so spending power ran on business hours and staffed counters, not on the traveler’s schedule.

Traveler’s checks relied on serialized paper stock and a global telegraphic ledger maintained by American Express. The issuing agent logged your first signature and check numbers; redemption clerks verified the second signature against that ledger via telex (the predecessor to fax) or phone before paying out.

“Think prepaid Visa gift cards before plastic. AmEx printed the value, and its global kiosk network redeemed it.”

What They Solved: Institutional Trust on the Road

American Express introduced the modern traveler’s check in 1891 after President J. C. Fargo discovered how hard it was to get cash abroad. The fix was simple and powerful: a pre-printed, dollar-denominated draft you signed at purchase and countersigned in front of the payee, who verified the match before acceptance.

That dual-signature scheme let AmEx reimburse lost checks while giving merchants bank-grade confidence. Because the face value stayed in hard currency and kiosks bearing the AmEx brand dotted more than 100 countries, travelers skipped local FX spreads and spent with a paper instrument the whole world trusted.

“Traveler’s checks showed the world that a strong brand guarantee can make paper spend like cash anywhere. Stablecoins take that same trust, strip out the branch counter, and settle the funds before the receipt even prints.”

Tony McLaughlin, Founder & CEO, Ubyx

What Still Broke: Manual Friction Everywhere

Traveler’s checks were trusted, but every step ran on human hours. To spend one, a traveler had to stand before a clerk who matched the second countersignature to the first; no clerk meant no redemption, which ruled out evenings, weekends, or remote towns.

Because each check was tied to the original buyer’s ID, it could not be passed along to a supplier or friend; secondary liquidity died at first spend. Clearing the paper was just as slow: bundles shipped overnight to regional ops centers before funds posted, leaving cash parked for days.

As payment cards and ATMs spread in the 1990s, travelers fled to faster rails and check volumes collapsed.

Debit Cards—Network Trust, Network Friction

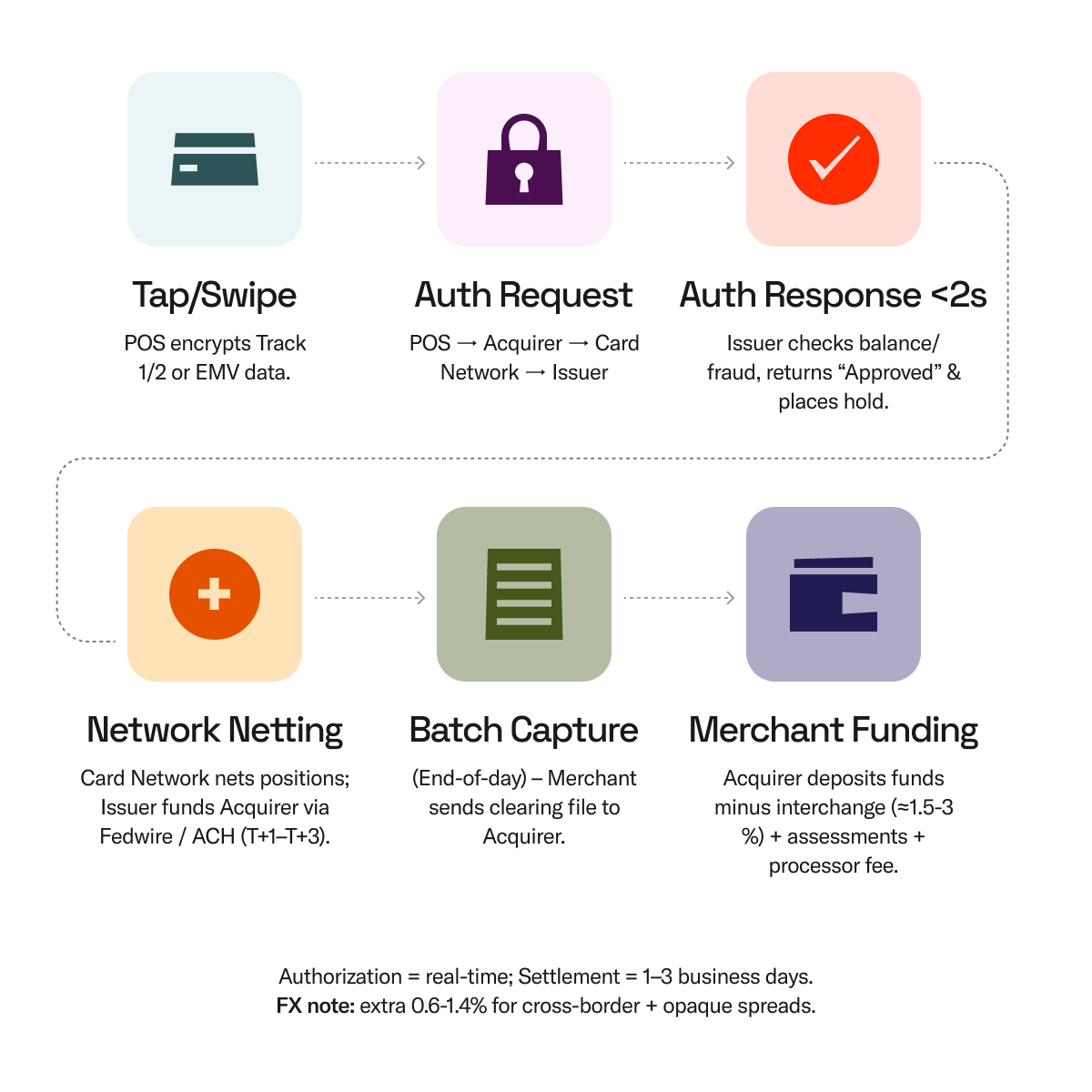

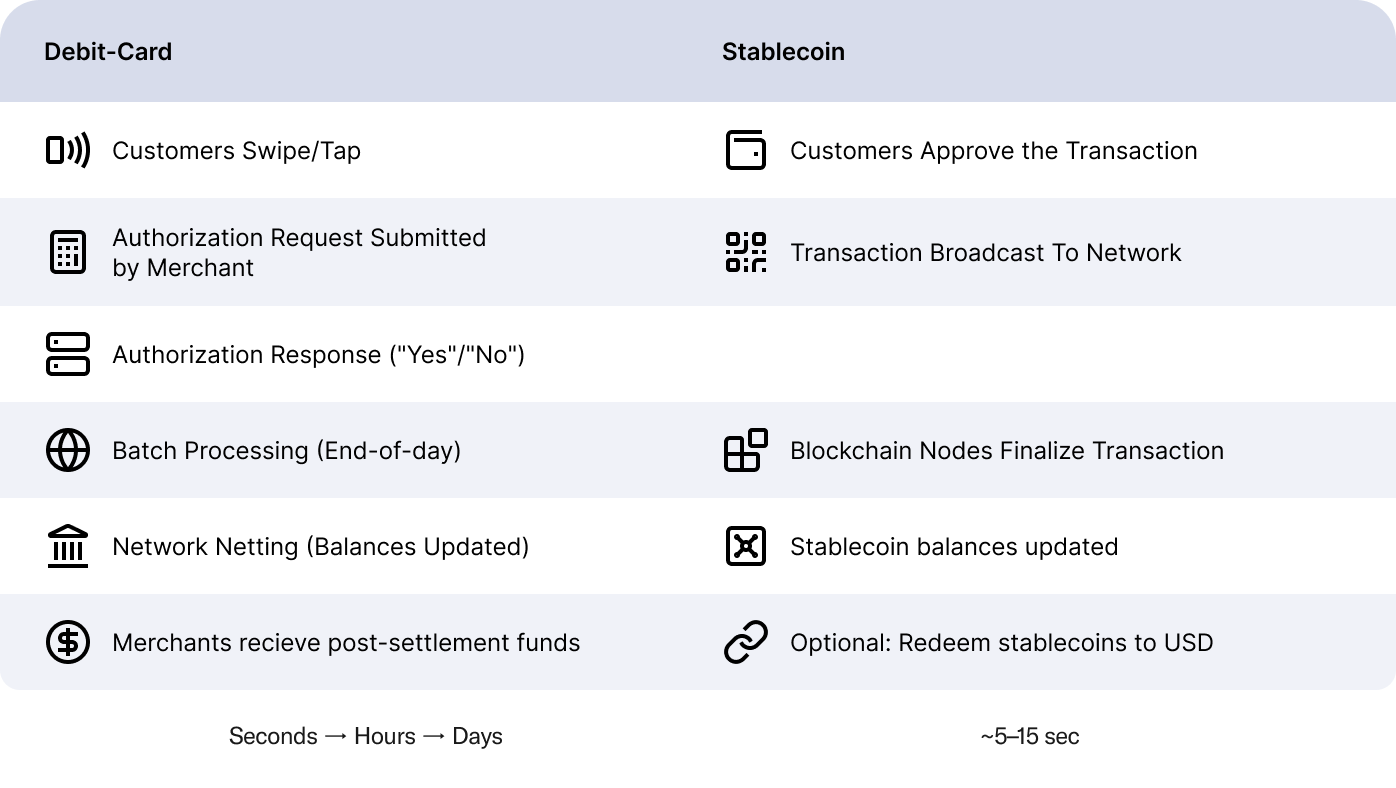

Debit cards pushed the ID check onto a real-time network. Each swipe got an instant “yes” or “no” but the cash still hitchhiked on 1970s batch files. Authorisation sped up; settlement never caught up, leaving merchants to bankroll float until the nightly processor sweep.

Magstripes stored account data that a point-of-sale terminal relayed over dial-up to VisaNet or Mastercard Banknet for an online “yes/no” in about five seconds. EMV chips, which were adopted in the mid-1990s, used public-key cryptography, shifting fraud checks onto the card itself while the four-party network kept batch settlement unchanged.

“Merchant payout delays on debit rails mirror the settlement drag that bearer bonds once bypassed.”

What They Solved: Credentialised Global Acceptance

Debit cards pushed trust online. A 1966 pilot at the Bank of Delaware showed that a mag-stripe linked to a checking account could clear funds in seconds, no clerk required. Visa’s nationwide programmes in the 1970s added the four-party network, issuer, acquirer, merchant and scheme, so one card worked almost everywhere a payment terminal blinked.

Real-time authorisation meant a swipe or chip tap delivered an instant yes-or-no, while “zero-liability” rules and FDIC-insured deposit backing turned the plastic into the safest way to spend a checking-account dollar.

What Still Broke: Legacy Float & Fee Gravity

Debit cards made the swipe feel instantaneous, but the cash still crept along 1970s batch rails. A sale doesn’t truly settle until the processor closes its nightly file and the network pushes funds through the clearing system. Merchants wait one to three business days for money to land in the bank.

During that wait, they also surrender margin. U.S. interchange now averages about 1.8 percent of every ticket, plus assessments from the network. Cross-border adds another toll booth. Visa layers an International Service Assessment of roughly 1.0–1.4% on foreign-issued cards before any FX spread appears.

Float isn’t the only capital sink. Chargebacks can claw back revenue up to 120 days after purchase, forcing processors to hold rolling reserves. Because business logic lives inside acquirer platforms, not the money itself, features like escrow, milestone payouts, or usage-based billing require custom middleware, add cost and integration risk.

In short, debit cards digitised the front-end tap but left merchants carrying settlement delay, fee drag, FX opacity, and limited programmability—the very frictions the next rail had to purge.

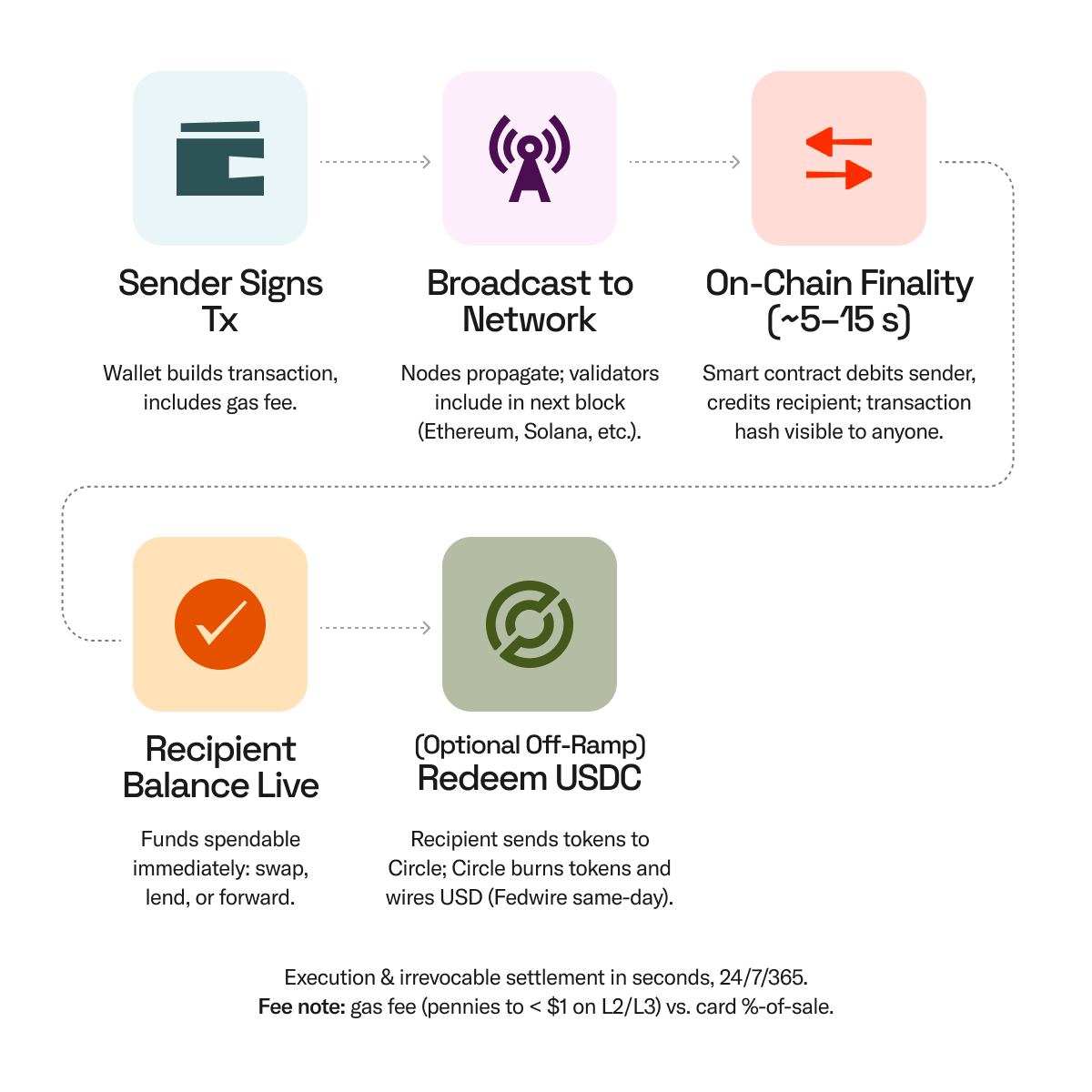

Stablecoins: Trust & Velocity, Written in Code

Stablecoins give you bank-grade backing, audited reserves, and a regulated issuer, while retaining the instant, bearer-style finality paper once promised. The trust lives in transparent balance sheets; the speed lives on a public ledger. No paper, no courier bags, no waiting.

Stablecoins run on public blockchains that are secured by public-key cryptography. Smart contracts handle token issuance, escrow, and compliance functions, while off-chain attestations flow in via APIs and oracles, enabling the asset to reconcile itself in real time, automatically, without a batch window.

“Just as traveler’s checks relied on AmEx’s global footprint, Circle and Visa are now building that same trust on-chain.”

What They Solve: Trusted Dollars at API Speed

A well-run stablecoin is a cash reserve wrapped in code. Issuers such as Circle post monthly attestations from Grant Thornton confirming every token is backed one-to-one by short-dated Treasuries or bank cash, giving holders the same “call-it-in-for-cash” certainty traveler’s checks once offered, only now the proof sits on a public ledger, not in a branch file.

The new GENIUS Act locks that discipline into law by requiring fully reserved “Permitted Payment Stablecoin Issuers” to publish those attestations on a fixed schedule. Because tokens ride open blockchains, value settles in seconds, 24/7, across borders. Visa’s 2023 pilot let Crypto.com send USDC over Ethereum to meet its daily VisaNet obligations, showing that a global network can close out positions without touching correspondent banks or SWIFT cut-off times.

For merchants and processors, float collapses and working capital stays productive instead of parking for T+2. DAOs push the concept even further: governance itself runs on programmable dollars.

A January 2025 MakerDAO executive vote set up automatic USDS payment streams of 25,402 USDS to aligned delegates and 122,438 USDS to core developers, directly from the treasury contract. This is all visible on-chain and was triggered the moment the proposal passed.

Risk Controls that Predecessors Lacked

Every stablecoin transfer is stamped onto a public ledger. Analytics firms and regulated off-ramps map those wallet addresses to verified customers, so investigators can follow funds in real time while user identities surface only at KYC endpoints; privacy for day-to-day commerce, transparency for courts and regulators.

Issuers also hold admin keys that let them comply with law-enforcement orders. Tether has frozen addresses linked to fraud and ransom payments; Circle routinely blocks or seizes USDC at wallets flagged for illicit activity. These controls turn a bearer bond-speed asset into one that authorities can still police.

Finally, the regulatory perimeter has caught up. Under the new GENIUS Act, a permitted payment stablecoin issuer must publish reserve attestations, maintain prudential capital, and operate under federal or qualified state supervision. These requirements are more stringent than the money-transmitter licences that governed early issuers.

In short, stablecoins fuse the immediacy of bearer paper with the compliance levers regulators demanded for decades but never had. Current on-chain payment solutions do face some challenges, however, when considering personal and protected information. Payroll data, for example, is intentionally separated such that employees aren’t able to see how much other employees make.

On-chain analytics could enable a sufficiently curious employee to untangle on-chain data from their employer and determine how much others at the company are making. Some projects are actively working to address such privacy considerations.

Money’s 200-year sprint shows a clear trajectory: we add trust, we add speed, and we prune whatever still drags. Bearer bonds nailed velocity but ignored accountability. Traveler’s checks institutionalised trust yet stalled at branch counters.

Debit cards digitised the handshake but left merchants feeding batch files and fee gravity. Stablecoins finally collapse the trade-off with audited, regulator-supervised dollars that settle in seconds and execute business logic on their own.